")

")

| Issue |

OCL

Volume 33, 2026

Oilseeds in Ukraine / Oléoprotéagineux en Ukraine

|

|

|---|---|---|

| Article Number | 19 | |

| Number of page(s) | 10 | |

| DOI | https://doi.org/10.1051/ocl/2026007 | |

| Published online | 28 April 2026 | |

Research Article

Analysis of the current state of oilseed production and processing in Ukraine☆

Institute of Oilseeds of the National Academy of Agrarian Sciences of Ukraine, Zaporizhia region

* Corresponding author: This email address is being protected from spambots. You need JavaScript enabled to view it.

Received:

6

December

2025

Accepted:

18

February

2026

Abstract

The main oilseed crops in Ukraine are sunflower, soybean, and rapeseed. The area under oilseeds exceeds 8 million hectares, or 39% of the total sown area. Sunflower crops—5 million hectares, soybeans—2 million hectares, rapeseed—1 million hectares. Ukraine ranks first in the world in terms of exports of sunflower, sunflower oil and meal, and rapeseed. The processing industry ranks first in Ukraine in terms of contributions to the state budget—16.7% of the total collection in 2024. In the 2023/24 season, record volumes of oilseeds were processed—17.4 million tons, 6.6 million tons of oil were produced, and 6.2 million tons were exported. For comparison, in the pre-war period of 2019/20 MY, these figures reached 6.9 million tons of production and 6.7 million tons of exports. Sunflower oil has been the export leader in Ukraine for the past 20 yr. The average annual production of sunflower oil is 5.4 million tons, with further exports of up to 5 million tons. Export revenue reaches $5 billion per year. The production and processing of soybeans is growing at the fastest pace. The processing industry of major oilseeds demonstrates the rapid adaptability of the processing industry during the period of transformations and sharp changes in operating conditions.

Résumé

Les principales cultures oléagineuses en Ukraine sont le tournesol, le soja et le colza. La superficie consommées d'oléagineux dépasse 8 millions d'hectares, soit 39 % de la superficie totale ensemencée. Tournesol - 5 millions d'hectares, soja - 2 millions d'hectares, colza - 1 million d'hectares. l'Ukraine se classe premier exportateur mondial de tournesol, d'huile et de tourteaux de tournesol, et de colza. L'industrie de transformation est la première en Ukraine en termes de contribution au budget de l'État - 16,7 % des recettes totales en 2024. Lors de la campagne 2023/24, des volumes records d'oléagineux ont été transformés - 17,4 millions de tonnes, 6,6 millions de tonnes d'huile produites, et 6,2 millions de tonnes exportées. À titre de comparaison, durant la campagne 2019/20 d'avant-guerre, ces chiffres atteignaient 6,9 millions de tonnes de production et 6,7 millions de tonnes d'exportations. L'huile de tournesol est le principal produit d'exportation ukrainien depuis 20 ans. La production annuelle moyenne d'huile de tournesol est de 5,4 millions de tonnes, avec des exportations supplémentaires pouvant atteindre 5 millions de tonnes. Les recettes d'exportation s'élèvent à 5 milliards de dollars par an. La production et la transformation du soja connaissent la croissance la plus rapide. L'industrie de transformation des principales oléagineuses démontre sa grande capacité d'adaptation face aux transformations et aux changements importants des conditions d'exploitation.

Key words: oil crops / crop area / sunflower / soybean / rape / processing

Mots clés : Cultures oléaginées / superficie cultivée / tournesol / soja / colza / transformation

Contribution to the Topical Issue: “Oilseeds in Ukraine / Oléoprotéagineux en Ukraine”.

© I. Chekhova, Published by EDP Sciences, 2026

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

This is an Open Access article distributed under the terms of the Creative Commons Attribution License (https://creativecommons.org/licenses/by/4.0), which permits unrestricted use, distribution, and reproduction in any medium, provided the original work is properly cited.

Highlights

As a result of the study, it was found that in Ukraine for 2000–2023 there is a tendency to increase the area of oilseed crops. Ukraine is the world leader in the production of sunflower oil in the world, with an indicator of over 5 million tons. The oilseed processing industry currently has to face a conjunction of military, political, land, economic, social, and environmental factors.

1 Introduction

The rapid growth of consumption and demand for vegetable fats has led to a sharp redistribution of sown areas in favor of oilseeds in the agricultural sector of Ukraine over the past 30 yr. The main oilseed crop is sunflower, the production of which is characterized by the highest level of profitability and liquidity. A leading trend has formed—sunflower occupies a leading position, rapeseed cultivation is restrained, and soybean production is reduced. The share of sunflower crops in the total area under all oilseeds is about 72%, the share of rapeseed crops is up to 13%, and the share of soybeans is about 15% (Chekhova, 2022).

Oilseed-derived vegetable oils and their constituent fatty acids are sources of renewable materials for industrial applications. Historically, vegetative oils derived from oilseed crops such as soybean and rapeseed have been used primarily for human consumption as frying oils, margarines, salad oils, and a variety of other food products (Zhu et al., 2016).

Sunflower gives the highest yield of oil per unit area. Sunflower oil accounts for 98% of the total oil production in Ukraine. Soybean is a valuable protein and oil crop that has a wide range of uses in feed production and the food industry. Rapeseed is grown in spring and winter, but winter rapeseed is of primary importance.

Similar trends are observed, e.g., in Serbia, where oilseeds account for about 10% of agricultural exports, and the best comparative advantages are observed in sunflower, both sunflower oil and sunflower seeds (Matkovski et al., 2025).

In Hungary, sunflower is the third most important crop in agriculture. The area under sunflower production has been increasing steadily over the past 20 yr. In 2024, Hungary rose to first place among European countries in sunflower cultivation for the first time, with a harvest of 1.7 million tons, which is 4.9% below the 5-yr average, a yield of 2.5 tons/ha, and an area of 680 thousand ha. The increase was due to higher yields: the average yield in Hungary increased by 53%. Sunflower oil production in Hungary will reach 951 thousand metric tons by 2026, which is 2.8% more than in 2021 (Chekhova and Fazekas, 2025).

Some countries, against the backdrop of increased domestic demand for vegetable oils, have been unable to solve the problem of increasing the production of oilseed raw materials for years due to low yields, logistics, etc.

India, as the world's largest oilseed producer, provides about 7–8 percent of the world's vegetable oil production. At the same time, it does not have time to meet domestic demand due to low yields, high production and market risks, and lack of irrigation. The country imports more than half of its oilseeds for domestic consumption (Sharma et al., 2017).

Tanzania has significantly increased production of oilseeds since 2010 but continues to import edible oil and processed oil-based products, while South Africa has established capabilities in crushing, refining, and manufacturing of oil-based products but imports oilseeds and edible oil mainly from Eastern Europe (Jahari et al., 2018).

Ukraine has become the largest exporter of sunflower oil in the world. Before the war, domestic companies sent about 200 thousand tons of sunflower oil to the EU market every month, which is an average of 35% − 45% of European consumption. Ukrainian vegetable oil and finished vegetable fats were sold by 760 companies in 155 foreign markets.

An in-depth study of secondary data highlights that Ukraine currently holds leading positions in global agricultural production and exports, including sunflower seeds, sunflower oil, rapeseed, and soybeans (Halkin, 2024).

Sunflower seed will remain a strategic crop in the UA agribusiness, ensuring the profitability of producers; sunflower seed and sunflower oil producers mainly have competitive price advantages; increasing the competitiveness of UA companies in domestic and foreign markets can be achieved by intensifying the technology of growing raw materials and optimizing costs; and diversification of products that are produced, namely high oleic oil, organic sunflower oil, and production using environmentally friendly technologies. EU countries became the largest importer of Ukrainian sunflower oil, more than 32% of total exports, according to Kuts and Makarchuk (2020).

In recent years, sunflower cultivation is one of the most highly profitable productions in agriculture. Sunflower seeds have a constant demand in different periods of the year, which indicates their high liquidity and export attractiveness. Moreover, to ensure the growth of sunflower cultivation, the concentration of crops in the regions with the most favorable conditions is of great importance (Petrenko et al., 2023).

With the beginning of the war, about 34 facilities in regions with active hostilities stopped their production.

Ukrainian agricultural producers suffer from the shelling of energy infrastructure facilities. This is explained by the fact that the power outage simply stops the work of enterprises or requires large expenses for the purchase of generators and other means that allow them to carry out their work in such conditions. In such conditions, it is worth mentioning that products from the oilseed market can become the basis of biomass for biofuel production. In this case, the problem of energy and fuel dependence can be solved (Shynkaruk and Kondratyev, 2024).

Therefore, ensuring sustainable development of the industry of processing seeds of major oilseeds becomes particularly urgent.

2 Materials and methods of research

Analysis of oilseed market indicators in Ukraine is presented in scientific publications by Kernasyuk (2019), Kulishov (2019), Kuts and Makarchuk (2020) and Halkin (2024). Taking into account the importance of the scientific results obtained, it should be noted that the issues of determining current trends and changes in production indicators of oilseed products and products of their processing remain insufficiently researched. The following methods were used in the research: systemic generalization, abstract-logical analysis and synthesis, observation, and comparison.

3 Analysis of the current situation in the industry and the dynamics of the production of raw materials and finished products

The domestic oil and fat industry has been developing dynamically over the past 20 yr, which required an appropriate level of supply of oilseeds. High demand for oilseed seeds contributed to the formation of a higher level of profitability of oilseeds and the expansion of sown areas. Thus, over the period 2000–2023, the area under oilseeds increased by 2.7 times: sunflower areas increased by 2 times, and sown areas of soybeans and rapeseed increased much more intensively—by 9.4 times. Significant potential for increasing oilseed production is concentrated in increasing their average yield. Thanks to the introduction of high-yielding hybrids, it was possible to achieve an increase in yield and oil content. According to the State Statistics Service, in the 2021/2022 season, farmers harvested a record harvest of oilseeds: sunflower—16.4 million tons, soybean—3.4 million tons, and rapeseed—2.96 million tons. Of these, processors produced 6.87 million tons of vegetable oil: sunflower—6.45 million tons, rapeseed—265 thousand tons, and soybean—163 thousand tons.

Ukrainian vegetable oil and finished vegetable fats are sold in 155 foreign markets and exported by 760 companies. 93% of the total volume of oil exports is supplied to four main regions: Europe, Southeast Asia, Asia, and the Middle East. Another 4% of revenues comes from the export of oils to African countries. In small quantities, Ukrainian oils are represented only in the territory of the Eurasian Economic Union countries, Australia, and the USA.

According to the State Customs Service of Ukraine, in 2020 Ukraine became the largest exporter of oil in the world. On the world market, competition for the first place among oil suppliers to India was waged with Russia, Argentina, Bulgaria, and Turkey. Competition in the Chinese market is made up of Russia, Kazakhstan, Bulgaria, and Argentina. Among the EU countries in 2020, the Netherlands became the largest importer. Among the suppliers to this country, Ukraine's competitors were Hungary, Spain, Belgium, and Portugal. Ukrainian companies sent about 200 thousand tons of sunflower oil to the EU market every month, which on average is 35% − 45% of European consumption.

Before the war in Ukraine, the vast majority of manufactured products were exported by sea. Due to active hostilities in the coastal territories, the work of Ukrainian ports in the Azov and Black Seas is currently suspended, and accordingly, farmers do not have the opportunity to freely sell their products by sea. Problems with exports have led to restrictions on the sale of products in the EU. For example, Spanish and Belgian supermarkets have begun to ration the sale of sunflower oil in the country per person per day. Rationing of exported products has begun to be introduced in Greece and Germany. In total, in Ukraine, according to Latifundist.com, there are about 70 sunflower processing plants, the basic capacity of which is 1,753,800 tons per month—about 58 thousand tons per day. With the beginning of the war in regions with active hostilities, about 34 facilities have stopped their production. For example, SEZs in the Kharkiv region and Odessa have stopped their work. Capacities also stopped in port cities: the satellite plant of the Chinese corporation COFCO stopped near Mariupol. Enterprises in the “hot” regions produced 29.3 thousand tons of products per day. Up to 20% of the capacities located in the territories with active hostilities belonged to multinational companies: Bunge, COFCO, Cargill, ADM, and Glencore. About 18% of the sunflower processing capacities belong to Kernel in the Kirovohrad, Kharkiv, Poltava, Odessa, and Mykolaiv regions.

Vegetable oil is one of the most demanded types of goods on both the domestic and international markets. Ukraine is the world leader in the production of sunflower oil. Other types of oilseeds, such as soybeans and rapeseed, are also grown in Ukrainian fields, but unlike sunflower, their domestic processing is still poorly developed. Currently, the production of sunflower oil is one of the most highly profitable types of business in Ukraine, so it would be appropriate to analyze the state, main trends, and prospects for the development of sunflower oil production in Ukraine (Bohdaniuk and Kicha, 2018).

Today, the main share of oil processing has passed to enterprises in regions without active hostilities, and the industry is transforming. Thus, in 2022, the largest processors of oilseeds are from the Kirovohrad, Vinnytsia, Lviv, and Poltava regions. Work in ports has stopped. The share of exports by land routes in Ukraine is quite low.

Despite active hostilities in some regions of Ukraine, there is enough capacity for oil production. Producers are already focusing on logistics when processing sunflower—the possibility of selling products. Given the situation in the country, it is impossible to determine which plants will resume their work after the end of the war.

Analysis of the balance of demand and consumption of oilseeds for 2021–2023 showed a decrease in initial stocks and residues of sunflower and rapeseed. Sunflower production decreased from 17.7 to 13.4 million tons, soybean production increased from 3.8 to 4.8 million tons, and rapeseed production increased from 3.1 to 4.2 million tons. Domestic consumption decreased from 12.9 to 12.5 million tons for sunflower, soybean consumption increased from 1.7 to 2.0 million tons, and rapeseed production increased from 445 to 463 thousand tons. Sunflower oil processing increased from 11.5 to 12.4 million tons. Sunflower exports decreased from 1.6 to 0.8 million tons, rapeseed exports increased from 2.7 to 3.7 million tons, and soybean production increased from 1.3 to 2.8 million tons. The balance of production and consumption of sunflower oil is positive. Thus, the volume of sunflower oil per year averages 5.4 million tons, with subsequent exports reaching up to 5 million tons (Tables 1–4).

According to the National Research Center “Institute of Agrarian Economics,” in 2023 the value of oilseed and fruit exports amounted to 2.8 billion USD. This is 25% less than in 2022. Rapeseed exports in natural terms decreased from 3.1 million tons in 2022 to 3.0 million tons in 2023, and soybean exports, on the contrary, increased by 1.5 million tons to 3.5 million tons. The most noticeable was the decrease in sunflower exports—from 2.8 million tons in 2022 to 0.8 million tons in 2023. The main buyers of Ukrainian oilseeds and oil in 2023, as in previous years, are European countries, as well as representatives of Asia. A characteristic feature of 2023 was the consolidation of the European Union's positions among the markets for the sale of fruits and seeds of domestic oilseeds. Last year, the countries of this region made about 70% of the value of purchases of all oilseeds from Ukraine. Germany, which lost first place to Romania in 2022, regained its leading position, taking 16.2% of Ukrainian exports of this type of agricultural product. Romania, with a share of 14.7%, moved to second place, pushing Turkey (13.4%) to third place in the ranking. Egypt, which in 2022 was not among the top 10 main buyers of domestic oilseeds, confidently took fourth place (11.0%). The share of the Netherlands in this ranking was 7.7% last year, and Poland—5.0%. In total, these six countries brought Ukraine 68% of export revenues from all foreign oilseed supplies.

There is a significant impact of trends in the world soybean market on the dynamics of production of this crop in Ukraine and a reduction in the lag in soybean production in Ukraine by dozens of times compared to the leaders in this industry (USA, Brazil, Argentina, China, and India). The production growth trends coincide with the trends of the leaders of the world soybean market in the USA, Brazil, and Argentina (Didenko, 2015).

In 2023, there was an increase in the volume of export supplies of soybean oil—298 thousand tons (+26%), and a multiple increase was recorded for rapeseed oil—379 thousand tons (+476%). In the group of oils and fats, sunflower oil remains the key commodity for export. In 2023, its exports from Ukraine amounted to 5.7 million tons—34% more than in 2022. Revenues from the sale of sunflower oil amounted to 5.0 billion USD, i.e., 8% less than in the previous year. Last year, a significant increase in the export of various oils in physical terms was accompanied by a reduction in the revenues of our profile companies in this segment. As in the case of cereals, the global decline in vegetable oil prices was felt, which was the largest among all food groups included in the FAO Price Index, reaching 33% in 2023.

The dynamics of sunflower, soybean, and rapeseed production for the period 2000–2023 is positive (Table 5.).

The increase in the area sown under sunflower was from 2.8 to 5.2 million hectares, winter rapeseed—from 0.09 to 1.4 million hectares, soybeans—from 0.06 to 1.8 million hectares, and spring rapeseed—from 58.3 to 48.6 thousand hectares. The maximum indicator of the area sown under sunflower was recorded in 2021 at 6.6 million hectares, soybeans in 2015 at 2.1 million hectares, winter rapeseed in 2019 at 1.2 million hectares, and spring rapeseed in 2010 at 101.6 thousand hectares. Sunflower production increased from 3.5 to 12.8 million tons, winter rapeseed from 0.1 to 4 million tons, soybeans from 0.06 to 3.4 million tons, and spring rapeseed from 31 to 67.7 thousand tons. The maximum production indicators of oilseed crops were achieved in 2021. Crop yields for the period almost doubled, the highest indicators for winter rapeseed.

The leaders in soybean cultivation by region in 2024 are Poltava (285.6 thousand ha), Khmelnytskyi (276.1 thousand ha), and Sumy (220.8 thousand ha). The largest areas of rapeseed are concentrated in Dnipropetrovsk (152.3 thousand ha), Odessa (110.8 thousand ha), and Vinnytsia (117.4 thousand ha). The leading regions in sunflower cultivation are Dnipropetrovsk (702.7 thousand ha), Kirovohrad (643.4 thousand ha), and Mykolaiv (486.5 thousand ha).

According to the results of 2024, 93% of soybean sowing areas are concentrated in enterprises and 7% in households; 99% of rapeseed sowing areas are concentrated in enterprises and 1% in households; and 85.8% of sunflower sowing areas are concentrated in enterprises and 14.2% in households (Table 6).

In Ukraine, according to the results of 2023, sunflowers were grown by 18,520 agricultural enterprises. The majority of them—10,840—have up to 100 hectares at their disposal. Analysis of sunflower production by agricultural enterprises by land area showed that the highest production productivity (up to 26.9 centners/hectare) is recorded in 136 enterprises with a land area of over 3000 hectares. Sunflower productivity in agricultural formations with a land area of up to 2000 hectares ranges from 22.3 centners/hectare to 25.8 centners/hectare. The lowest sunflower productivity in agricultural formations with a land area of up to 100 hectares is 22.3 c/h (Table 7).

In Ukraine, according to the results of 2023, soybeans were grown in 9972 agricultural enterprises: 7092 have up to 100 hectares at their disposal. The highest production productivity (up to 29.1 c/ha) is recorded in 127 enterprises with a land area of over 2000–3000 hectares. Soybean yield in agricultural formations with a land area of up to 2000 hectares is from 22.5 c/ha to 28.3 c/ha. The lowest soybean productivity in agricultural formations with a land area of up to 100 hectares is 22.5 c/ha (Table 8).

According to the results of 2023, rapeseed was grown by 6037 agricultural enterprises. The majority of them—2971—have up to 100 hectares at their disposal. The highest production productivity (up to 31.6 centners/hectare) is recorded in 244 enterprises with a land area of over 1000 hectares. Rapeseed yield in agricultural formations with a land area of up to 1000 hectares is from 27.2 centners/hectare to 28.6 centners/hectare. The lowest sunflower productivity is in agricultural formations with a land area of up to 100 hectares (Table 9).

According to the directory of processors “Tripoli-land,” the largest oilseed processors are concentrated in the south of the country. Oilseed processors with sunflower oil production volumes of over 200 thousand tons of oil per year: LLC “European Transport Stevedoring Company” (Mykolaiv region), Allseeds Black Sea (Odesa region), Prydniprovsky MEZ (Kirovohrad region), Kakhovka branch of LLC “AT Cargill” (Kherson region), PJSC Z II “DOEZ” (Dnipropetrovsk region).

During the 2023/2024 MY, soybeans were exported in the amount of almost 3 million tons worth $1.1 billion, with a harvest of 4.9 million tons. Rapeseed: 3.7 million tons worth $1.4 billion, with last year's production of 4.5 million tons, and sunflower: 300 thousand tons. In the group of oils and fats, sunflower oil remains the key commodity for export. In 2023, sunflower oil exports from Ukraine amounted to 5.7 million tons—34% more than in 2022. Revenues from the sale of sunflower oil amounted to 5.0 billion USD. Sales are carried out by 760 companies in 155 foreign markets.

Dynamics of the balance of demand and consumption of sunflower, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of rapeseed, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of soybeans, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of sunflower oil, in thousand tons, 2021–2023*.

Dynamics of sunflower, soybean, and rapeseed production in 2000–2023.*

Sown areas of main oilseed crops by management form, 2024.*

Grouping of enterprises by the size of the harvested sunflower area, 2023.*

Grouping of enterprises by size of harvested soybean area, 2023*.

Grouping of enterprises by the size of the harvested rapeseed area, 2023.*

4 Features of the functioning of the main oilseed processing industry

The work of business entities under martial law due to full-scale Russian aggression suffered significant obstacles to the sustainable development of the industry, including emergency and fan power outages; logistical problems associated with the functioning of the grain corridor; shelling and destruction by the aggressor of port infrastructure; and blocking of road transport checkpoints on the western border. At the same time, in the 2023/24 season, record volumes of oilseeds were processed—17.4 million tons (of which 14.8 million tons are sunflower, 1 million tons are rapeseed, and 1.6 million tons are soybean). This indicates the rapid adaptability of the main oilseed processing industry during the period of transformations and sharp changes in operating conditions.

The processing industry ranks first in Ukraine in terms of contributions to the state budget. According to the State Tax Service, 16.7% of the total collection to the Consolidated Budget of Ukraine for the three quarters of 2024 falls on wholesale and retail trade (16%), public administration and defense (11.3%), and financial and insurance activities (10.9%). The strategic goal is to modernize the structure of the Ukrainian economy and increase the share of the processing industry from the current 8%–10% to 20%. The Made in Ukraine program is aimed at supporting and developing Ukrainian producers and includes three areas: developing domestic production, attracting investment in the real sector, and supporting non-raw material exports. Among the tools are grants for the development of the processing industry (uaprom.info, 2025). The grant program on the Diya portal for processing enterprises of individual entrepreneurs (FOPs) and legal entities provides businesses with the opportunity to receive financial support for the development of their companies. The main conditions of the program are the obligation to create new jobs and co-finance the project. The grant recipient must ensure the creation of up to 25 jobs, which contributes to the development of the economy and employment. And co-financing is distributed according to the scheme: the recipient must contribute 50% of his own funds, and the state provides the remaining 50% in the form of a grant. For enterprises operating in the deoccupied territories, co-financing is 20% from the entrepreneur and 80% from the state. Since the start of the program, more than 400 grants have already been issued for 2.2 billion UAH.

Reduction in processing capacity as a result of military operations. Before the full-scale invasion, oilseed processing capacity in Ukraine was at the level of 24 million tons. Over the past two years, according to various estimates, processing capacity has decreased to 21 million tons. Some of the SEZs in the eastern and southeastern regions have been lost.

Reduction in the area sown to oilseeds, and therefore the gross harvest, which provoked a capacity surplus in 2021–2022. The capacity surplus stimulates processors to increase processing at the expense of traditionally export-oriented crops—soybeans and rapeseed. And this is 8.7 million tons of additional raw materials. Most oil extraction plants are insured and install equipment for processing at least two oilseeds, and ideally three. Thus, for the first time in the history of Ukraine, 1 million tons of rapeseed were processed, which is 22.3% of the total harvest in 2023 and 0.8 million tons more than in previous periods. This is especially important since rapeseed is usually an export-oriented crop. Rapeseed oil production reached a record 430,000 tonnes, while exports of this product increased by 404%, reaching 424,000 tonnes.

According to some market researchers, EU demand for Ukrainian rapeseed will grow due to an increase in the share of renewable energy in gross final energy consumption, which will reach 45% by 2030 according to the REPowerEU plan, which predicts an increase in demand for biodiesel (Makarchuk, 2025).

There is also an increase in the production and export of soybean oil and meal—by 22% and 29%, respectively. European market remains a key priority. Ukrainian soybeans are in high demand in the EU, thanks to short logistics routes and fast cash turnover. Poland serves as the first link in this supply chain, creating additional opportunities for small and medium-sized producers who rely on quick payment cycles (ukraine-pulse.org, 2025). In total, record volumes of the main types of oilseeds were processed last season—17.4 million tons.

The trend in recent years is to shift oilseed processing to the western regions and to process three strategic crops: sunflower, rapeseed, and soybeans. Thus, in May 2025, the VITAGRO group of companies began sequential processing of three strategic crops: sunflower, rapeseed, and soybeans. This decision is the implementation of a long-term strategy of diversification of production, increasing operational flexibility, and strengthening the company's position in the vegetable oils and meal market. The new soybean processing line, with a capacity of 250 tons per day, allows us to significantly expand the product range and strengthen the competitiveness of the plant (agrotimes.ua, 2025).

Large oilseed processors, such as Kernel, Korolivskyi smak, Ukroliya, and Astarta, have their own sowing areas. That is, they are able to provide themselves with part of the raw materials and purchase part on the market. And other processors will follow this path in the future.

Sunflower remains the most popular crop. In each region, there is an increase in the volume of oilseeds, because the emphasis on their production allows for maximum use of the geographical location and available technical resources to increase the competitiveness of both the region and its individual entities. Thus, in the 2023/24 MY, oil and fat industry enterprises produced 6.6 million tons of sunflower oil and exported 6.2 million tons to foreign markets, which was the second-best result in all years of work. The volume of production and export of sunflower oil was greater only in the 2019/20 MY (6.9 million tons and 6.7 million tons, respectively). And compared to the pre-war 2020/21 MY of the last season, the volumes of production and export increased by 13.7% and 17%, respectively. The increase in sunflower oil production was facilitated by a significant increase in sunflower seed processing at domestic facilities due to a significant reduction in its exports (compared to 2022/23 MY, a reduction of 83.4%, or 1.5 million tons). In the reporting period, 14.8 million tons of sunflower seeds were processed into oil, which is 1.3 million tons more than in 2022/23 MY.

The specificity of the oilseed processing industry is characterized by relative stability and a high level of adaptability to market conditions. This is ensured due to the special importance of food in the life of the population, the export-oriented nature of finished products, the high liquidity of food products, and the developed infrastructure.

5 Impact of the invasion

Agriculture is the central pillar of the Ukrainian economy and a major source of livelihood for about one-third of the Ukrainian population. The abundant fertile land, suitable climatic conditions, and a relatively favorable investment climate have made Ukraine able not only to feed itself but also to provide food for millions of people in Asia, Africa, the Middle East, and other countries. Before the war, agriculture was one of the fastest-growing sectors in Ukraine (with an annual growth of 5%–6%), contributing 10.9% of GDP and providing 17% of domestic employment by 2021 (Mamonova et al., 2023).

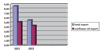

It should be noted that in 2021, oil exports from Ukraine reached the following indicators: total revenue amounted to about 8.56 billion dollars, and sunflower oil exports amounted to 5.1 million tons worth 6.4 billion dollars. Revenues increased due to high prices. Ukraine also increased exports of rapeseed and soybean oils, which made this sector key for the Ukrainian economy, occupying a significant share in agricultural exports. In 2022, sunflower oil exports from Ukraine amounted to about 4.3–4.6 million tons, which was 16% less than in the previous year, and the total value of exports amounted to about 5.5 billion dollars (Fig. 1).

Before the war in Ukraine, the majority of manufactured goods were exported by sea. Due to active hostilities in the coastal territories, the work of Ukrainian ports in the Azov and Black Seas is currently suspended, and accordingly, farmers have no opportunity to freely sell their products by sea.

The main share of oil processing has passed to enterprises in regions without active hostilities, and the industry is transforming. Thus, in 2022, the largest processors are oil processing plants from the Kirovohrad, Vinnytsia, Lviv, and Poltava regions. Work in ports has stopped.

A market study was conducted of the current state of production and processing of sunflower, soybean, and rapeseed in Ukraine for the period 2021–2023. An analysis of the balance of demand and consumption of oilseed crops for 2021–2023 showed a decrease in initial stocks and residues of sunflower and rapeseed. Sunflower production decreased from 17.7 to 13.4 million tons, soybean production increased from 3.8 to 4.8 million tons, and rapeseed production increased from 3.1 to 4.2 million tons. Domestic consumption decreased from 12.9 to 12.5 million tons for sunflower, soybean consumption increased from 1.7 to 2.0 million tons, and rapeseed production increased from 445 to 463 thousand tons. Sunflower oil processing increased from 11.5 to 12.4 million tons. Sunflower exports decreased from 1.6 to 0.8 million tons, rapeseed exports increased from 2.7 to 3.7 million tons, and soybean production increased from 1.3 to 2.8 million tons. The average annual production of sunflower oil is 5.4 million tons, with further export—up to 5 million tons.

Some regions are heavily dependent on imports of Ukrainian agri-food commodities. Northern Africa and Western Asia are among them. More than 11% of domestic use of oil crops and 17.5% of domestic consumption of vegetable oils was also covered by imports. Regarding oil crops and oils, a relatively high dependency of domestic use on imports was also observed in Central Asia and Western and Northern Europe. Those regions seem to be most at risk of deterioration in food security in the case of a possible reduction in supplies from Russia and Ukraine as a result of a prolonged conflict (Hamulczuk et al., 2023).

The main feature of the oil and fat industry of Ukraine, as for the entire country, remained working under martial law due to the full-scale aggression of Russia. Enterprises faced numerous obstacles, including emergency and fan power outages, logistical problems associated with the functioning of the grain corridor, attempts by the aggressor to destroy port infrastructure, blocking of road transport checkpoints on the western border, periodic application of conventions on restrictions or prohibitions on product shipments, etc. Despite the negative and sharp changes in organizational, logistical, and pricing mechanisms for the period 2022–2024, there are positive dynamics and a recovery of negative indicators of raw material supply and demand in the oilseed processing industry.

Research shows that the full-scale invasion affected not only the fluctuations of global GDP but also, with some delay, global supply chains, which indicates a deepening of differences in the logistics sector. Industries dependent on global logistics supply chains have proven to be very sensitive to changes in the flexibility of transformation and changes in the configuration of supply chain networks. It has been established that the consequences of the unrest in Ukraine have exacerbated the financial, humanitarian, food, energy, social, and vital crises. As for the impact on the Ukrainian logistics sector, they have led, among other things, to the weakening/breaking of logistical ties, the lack of potential for their full use during wartime, and increased security threats (Krykavskyy et al., 2023).

|

Fig. 1 Export flows of the processing industry of Ukraine before and after the invasion, billions of dollars, 2021-2022. |

Conclusions

The oil and fat industry of Ukraine has formed a powerful production and export vector of economic development over the past 20 yr. Stable demand for sunflower, soybean, and rapeseed seeds and their processing products contributed to the formation of a high level of profitability of oilseeds and the expansion of the sown areas for their production.

Thus, over the period 2000–2023, the area under oilseeds increased by 2.7 times: the area under sunflower increased by 2 times, and the area under soybean and rapeseed increased by 9 times. The increase in the area under sunflower was from 2.8 to 5.2 million hectares, winter rapeseed—from 0.09 to 1.4 million hectares, soybean—from 0.06 to 1.8 million hectares, and spring rapeseed—a decrease in the area from 58.3 to 48.6 thousand hectares. The maximum area of sunflower crops was recorded in 2021 at 6.6 million hectares, soybeans in 2015 at 2.1 million hectares, winter rapeseed in 2019 at 1.2 million hectares, and spring rapeseed in 2010 at 101.6 thousand hectares. Sunflower production increased from 3.5 to 12.8 million tons, winter rapeseed from 0.1 to 4 million tons, soybeans from 0.06 to 3.4 million tons, and spring rapeseed from 31 to 67.7 thousand tons.

Significant potential for increasing oilseed production is concentrated in increasing yields by almost twofold. Thus, sunflower yield increased from 12.2 to 24.5 c/ha, soybeans from 10.6 to 25.9 c/ha, and rapeseed from 10.3 to 29.5 c/ha. Analysis of sunflower production by agricultural enterprises showed that the highest production productivity—26.9 c/ha—was recorded in 136 enterprises with a land area of over 3000 ha. The highest soybean yield—29.1 c/ha—was recorded in 127 enterprises with a land area of over 2000 ha. The highest rapeseed production productivity at 31.6 c/ha was recorded in 244 enterprises with a land area of over 1000 ha.

It was established that over 90% of the gross production of soybeans and rapeseed and 86% of sunflowers in Ukraine is provided by agricultural enterprises. Households grow up to 7% of soybeans, 1% of rapeseed, and 14% of sunflowers.

Ukraine is the world leader in the production of sunflower oil.

The balance of production and consumption of sunflower oil is positive. The volume of sunflower oil per year averages 5.4 million tons, with further exports of up to 5 million tons. The volumes of soybean and rapeseed oil are growing rapidly. In 2023, soybean oil exports increased by 26% to 298 thousand tons, and rapeseed oil by 4.7 times to 379 thousand tons.

Ukrainian vegetable oil and finished vegetable fats are sold in 155 foreign markets and are exported by 760 companies. 93% of total oil exports are supplied to four main regions: Europe, Southeast Asia, Asia, and the Middle East; 4% to African countries.

It has been determined that the current problem of the development of the oil processing industry of the main oil crops is due to military, political, land, economic, social, and environmental factors. Military operations in the country create logistical and production problems for the development of production and processing of the main oil crops. But the specifics of the oil processing industry are characterized by relative stability and a high level of adaptability to market and crisis conditions.

This is ensured by the special importance of oils in human nutrition, the export-oriented nature of finished products, the high liquidity of food products, and the developed infrastructure. The following factors contributed to this: high profitability of growing oil crops, modernization of processing capacities, and established export of oil crops to 155 countries of the world.

References

- Analysis of the market of oilseeds and processed products (sunflower, soybean, rapeseed) in Ukraine. 2022. Available from: https://pro-consulting.ua/ua/issledovanie-rynka/analiz-rynka-maslichnyh-kultur-i-produktov-pererabotki-podsolnechnik-soya-raps-v-ukraine-2022-god (last consult: 03/12/2025). [Google Scholar]

- Bohdaniuk OV, Kicha AO. 2018. Assessment of the state of sunflower oil production in Ukraine: main trends and prospects. https://economyandsociety.in.ua/journals/19_ukr/207.pdf. doi: https://doi.org/10.32782/2524-0072/2018-19-207 (last consult: 03/12/2025). [Google Scholar]

- Balances. USDA. World Grains and Oilseeds Market September 2025. https://uga.ua/balansi/ (last consult: 03/12/2025). [Google Scholar]

- Chekhova IV. 2021. Formation and development of the oilcrop market: theory, methodology, practice. Monograph. Kyiv: Agrarna nauka, p. 144 [Google Scholar]

- Chekhova IV. 2022. Features of the functioning of the oilcrop market in Ukraine. Sci. Tech. Bull. Inst. Oilseeds Natl. Acad. Sci. 32: 154–161. doi: 10.36710/IOC–2022–32–15. [Google Scholar]

- Chekhova IV. 2022. Sunflower is the main oilseed crop in Ukraine. Helia. 45: 167–174. https://:doi.org/10.1515/helia-2022-0007. [Google Scholar]

- Chekhova I, Fazekas M. 2025. Production and consumption of sunflower seeds in Hungary. In: Oilseed crops: present and prospects. Collection of abstracts of the International Scientific Internet Conference. Zaporizhzhia: IOK NAAS, pp. 114-116. http://imk.zp.ua/index.php/konferentsii-seminary-dni-polia/489-26-2025. [Google Scholar]

- Didenko N. 2015. Prospects of Ukrainian soybean on the eu market. Econ. Manag. APC.1. Available from: https://econommeneg.btsau.edu.ua/en/content/perspektivi-ukrayinskoyi-soyi-na-rinku-ies-prospects-ukrainian-soybean-market-eu. (last consult: 03/12/2025). [Google Scholar]

- Halkin V. 2024. The Role of Ukraine in Ensuring Global Food Security: Current challenges and prospects. Grassroots J. Nat. Resour. 7: 396-419. doi: https://doi.org/10.33002/nr2581.6853.0703ukr20 [Google Scholar]

- Hamulczuk M, Pawlak K, Stefanczyk J, Colebiewski, J. 2023. Agri-food supply and retail food prices during the Russia–Ukraine conflict's early stage: implications for food security. Agriculture 13: 2154. https://doi.org/10.3390/agriculture13112154. [Google Scholar]

- Jahari C, Kilama B, Dube S, Paremoer T. 2018. Growth and development of the oilseeds-edible-oils value chain in Tanzania and South Africa. Available from: https: doi:10.2139/ssrn.3115940. [Google Scholar]

- Krykavskyy Y, Shandrivska O, Pawłyszyn I. 2023. A study of macroeconomic and geopolitical influences and security risks in supply chains in times of disruptions. LogForum 19, 423-441. http://doi.org/10.17270/J.LOG.2023.855. [Google Scholar]

- Kysylevsky. The processing industry has become a leader in contributions to the state budget. Available from: https://uaprom.info/news/pererobna-promyslovist-vyjshla-v-lidery-za-vidrakhuvanniamy-do-derzhbiudzhetu-kysylevskyj/ (last consult: 03/12/2025). [Google Scholar]

- Kernasyuk Y. 2019. Rapeseed production and processing industry: opportunities, prospects. Available from: http://agro-business.com.ua/agro/ekonomichnyihektar/item/18109-industriia-vyrobnytstva-i-pererobky-ripaku-mozhlyvostiperspektyvy/ (last consult: 03/12/2025). [Google Scholar]

- Kulishov D. 2019. Soybean stocks in Ukraine: current situation. Available from: https://mizez.com/news/zapasi-so-v-ukran-aktualna-situatsya. (last consult: 03/12/2025). [Google Scholar]

- Kuts Т, Makarchuk О. 2020. Ukrainian Sunflower Market on the Background of EU and US Markets. Probl. World Agric. 20: 4–15. DOI: 10.22630/PRS.2020.20.3.13 [Google Scholar]

- Matkovski B, Djokic D, Zekic S, Jurević J. 2025. Competitiveness of oilseed production: evidence from Serbia. Front. Sustain. Food Syst. 9: 1–11. https://doi.org/10.3389/fsufs.2025.1651410. [Google Scholar]

- Mamonova N, Borodina O, Kuns B. 2023. Ukrainian agriculture in wartime. Resilience, reforms, and markets https://www.tni.org/en/article/ukrainian-agriculture-in-wartime. (last consult: 03/12/2025) [Google Scholar]

- Makarchuk O, Kuts T, Labenko O, Kuts O. 2025. Market evaluation of rapeseed in Ukraine: perspectives and challenges. Sci. Pap. Ser. Manag. Econ. Eng. Agric. Rural Dev. 24: 505–514. https://www.researchgate.net/publication/397940825_MARKET_EVALUATION _OF_RAPESEED_IN_UKRAINE_PERSPECTIVES_AND_CHALLENGES. (last consult: 03/12/2025). [Google Scholar]

- Petrenko V, Topalov A, Khudolii L, Honcharuk Y, Bondar V. 2023. Profiling and geographical distribution of seed oil content of sunflower in Ukraine. Oil Crop Sci. 8: 111-120. https://doi.org/10.1016/j.ocsci.2023.05.002. [Google Scholar]

- Potaeva O. VITAGRO has started multicultural processing. Available from: https://agrotimes.ua/elevator/vitagro-rozpochav-multykulturnu-pererobku/ (last consult: 03/12/2025). [Google Scholar]

- Sharma V. 2017. Overview of the oilseed sector: current status and growth trends. In: Oilseed production in India. New Delhi: Springer. 215: 3–9. https://doi.org/10.1007/978-81-322-3717-4. [Google Scholar]

- Shynkaruk L, Kondratyev Y. 2024. Current state of development of the oilseed market in Ukraine: main trends and influencing factors. Curr. Probl. Econ. 2: 83-90. doi: 10.32752/1993-6788-2024-2-282-83-90. [Google Scholar]

- Ukrainian soybeans and peas prepare for new export regulations—key takeaways from the Soybean and Meal Market Conference. Available from: https://ukraine-pulse.org/en/news/ukrainian-soybeans-and-peas-prepare-for-new-export-regulations-%E2%80%94-key-takeaways-from-the-soybean-and-meal-market-conference/(last consult: 03/12/2025). [Google Scholar]

- Zhu L-H, Krens F, Smith MA, et al. 2016. Dedicated industrial oilseed crops as metabolic engineering platforms for sustainable industrial feedstock production. Sci. Rep. 6: 22181. https://www.nature.com/articles/srep22181. [Google Scholar]

Cite this article as: Chekhova I., 2026. Analysis of the current state of oilseed production and processing in Ukraine. OCL 33: 19. https://doi.org/10.1051/ocl/2026007

All Tables

Dynamics of the balance of demand and consumption of sunflower, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of rapeseed, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of soybeans, in thousand tons, 2021–2023*.

Dynamics of the balance of demand and consumption of sunflower oil, in thousand tons, 2021–2023*.

All Figures

|

Fig. 1 Export flows of the processing industry of Ukraine before and after the invasion, billions of dollars, 2021-2022. |

| In the text | |

Current usage metrics show cumulative count of Article Views (full-text article views including HTML views, PDF and ePub downloads, according to the available data) and Abstracts Views on Vision4Press platform.

Data correspond to usage on the plateform after 2015. The current usage metrics is available 48-96 hours after online publication and is updated daily on week days.

Initial download of the metrics may take a while.